By Ivy Schmerken, Editorial Director

The appetite for multi-leg options strategies is on the rise.

But this also means capturing liquidity that is fragmented across multiple options exchanges.

Complex orders or spread trades allow traders to simultaneously buy or sell a number of different options in what otherwise would require separate orders.

“The vast majority [of complex orders] have two or three individual series that are legs of a complex order and most of those are generated by the end user,” explains Boris Ilyevsky, managing director at International Securities Exchange. ISE and CBOE are viewed as the leaders and are said to operate the largest complex order books.

Historically, multi-leg orders were executed manually through brokers and by picking up the phone. However, the ability to execute these orders electronically through electronic complex order books has only gained traction in the past five years.

The availability of front-end tools, such as execution management systems (EMS), that scan complex order books and aggregate liquidity across multiple exchanges have leveled the field among asset managers and hedge funds.

“Multi-leg orders have become a huge part of the options market,” according to Andy Nybo, principal and head of derivatives research and consulting at TABB Group. “Partly it’s the ability to increase these complex orders using technology and electronic tools that facilitate these orders,” says Nybo. More than that, those implementing and developing these strategies can obtain significant advantages when they package orders together.

Savvy investors and traders are looking to earn more ‘edge’ from their trades or to construct better hedges. The lower cost of hedging and the chance for higher returns are drivers behind the trend, says Nybo.

Even retail investors are being given web front-ends that they can use to line up the legs of an options trade with the NBBO. (see sidebar)

Executing Complex Orders

There are two basic ways that complex orders are executed:

- When a complex order arrives on the order book, other market participants become aware of it and they respond to it by putting in a complex order of their own on the opposite side, explains Ilyevsky. Whoever hits it first trades with them.

- If a complex order arrives on the book but no one is interested, the order is maintained until someone responds. Or, when the net prices match up, the individual series of the order can leg into the regular order book.

The benefit of “legging in” to the regular order book is that complex orders can access the full liquidity of the exchange’s regular order book, according to ISE officials. The fill rates are likely to be higher.

But the visibility into electronic systems housing complex orders has not always been so transparent.

In the past, complex orders would sit in the complex order book and there was no interaction between the order book and the listed quotes. “You have 12 markets and they’re all quoting all the time,” observes Henry Schwartz, CEO of Trade Alert.

In addition, because complex orders could contain three or more sides, it can be difficult to execute the entire order simultaneously.

According to Tabb Group’s US Options Trading 2014/2015 report, “The Buy Side’s Insatiable Thirst for Liquidity,” 42 percent of institutions participating in the survey cited less liquidity as the major change over the past year.

Because finding the other side of the trade is challenging, buy side firms are looking to front-end trading tools to access complex order books. In the Tabb Group options survey, 36 percent of those responding said that front-ends need to support complex order capabilities.

Fragmentation

Executing complex orders can be challenging since traders must access fragmented liquidity across seven complex order books. This trend has led to the evolution of sophisticated algorithms and more tools that scan complex order books for liquidity.

“It’s getting easier and the capabilities for executing complex orders are evolving,” comments Trade Alert’s Schwartz.

First, customers are able to access the complex order books more readily through brokerage front-ends, notes Schwatz. And second, exchanges are getting more sophisticated in terms of what they will let you do,” he adds.

Exchanges

Spread trading is also driving order flow to US options exchanges. ISE was the first exchange to launch a complex order book (known as ISE Spread Book) in 2002, followed by CBOE with its COB in 2005.

Four other exchanges also operate complex order books —CBOE’s C2, Nasdaq OMX, PHLX, NYSE Amex and Arca and BOX. Many expect that number to rise. Reportedly, MIAX is said to be working on a complex order book, and while BATS does not currently operate one, options insiders would not be surprised to see that change.

Retail Investors Dive into Complex Orders

Online brokers paved the way for multi-leg options trading among retail investors, supplying them with front-end tools and widgets to set up complex orders. In fact, the popularity of multi-leg options trading has been a force in propelling many acquisitions in the online options brokerage space. Both Schwab and TD Ameritrade acquired options specialists known for pioneering multi-leg orders to retail investors. Schwab bought OptionsXpress while TD Ameritrade purchased Think or Swim. In addition, OptionsHouse and tradeMonster recently merged.

“The larger firms wanted a toehold in multi-leg spread trading without have to build the technology from scratch,” wrote the author of “Simple Agenda for Complex Options” in Futures Industry Magazine.

Even more generic retail-oriented shops have rolled those tools out to main street investors, according to Andy Nybo, TABB Group’s principal and head of derivatives research and consulting. So it’s not only high performance front-ends that sophisticated traders use; it’s also simple web-based tools that allow retail investors to trade that way, emphasizes Nybo.

But retail investors are not interacting with the complex order books or subscribing to the proprietary complex order book data feeds.

In terms of executing complex orders, retail brokers rely on order routing partners or aggregators – the likes of Citadel, Susquehanna and Citi for equity and equity options order flow. These consolidators tend to look to the complex order books and subscribe to those feeds to make routing decisions based on what’s residing on the books. “The retail broker always looks for best execution and price improvement. The routing firm is routing to various exchanges to find which are displaying the best price,” says Nybo. “If they get price improvement for the retail brokers, the retail brokers love that. That’s what distinguishes the wholesalers,” says Nybo.

But wholesalers are not the only ones in the game. The ecosystem for complex orders involves market makers and high frequency trading firms investing in low-latency infrastructure and platforms.

“Retail orders get filled because of HFT and market makers that are actively monitoring the market and actively responding to complex orders,” says Boris Ilyevsky, managing director at International Securities Exchange. “Professional market makers and liquidity providers actively seeking to connect with incoming orders are constantly tweaking their platforms and trying to get faster,” says Ilyevsky. Manual executions occur on the retail and institutional sides of the business, he says. However, those competing against large market making firms are operating in a completely automated fashion.

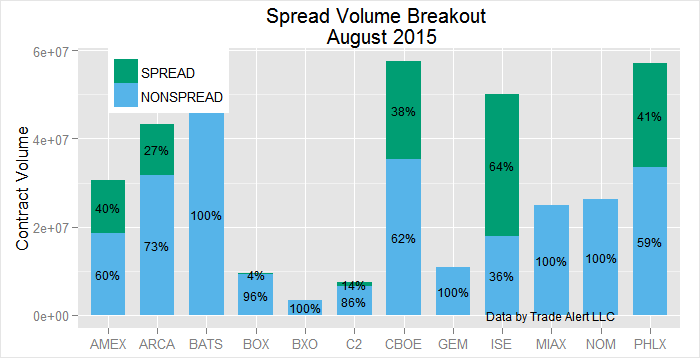

Since the business is so competitive, exchanges do not break out their complex order volumes. It’s estimated that complex orders account for 30 to 40 percent of industry-wide options volumes. Some exchanges are surpassing those percentages. In August, ISE earned 64% of its volume from spread trades, vs. 36 % from nonspread trades, according to data from Trade Alert LLC. As a point of comparison, CBOE generated 38% of its volume from spread trades and 62 % from nonspreads, while Amex earned 40% from spreads, 60 % from nonspreads, while Arca earned 27% of its volume came from spreads and 73 % from nonspreads, while PHLX earned 41% from spreads and 59% from nonspreads. However, it’s also possible to execute spread trades outside of the complex order book.

(Click Chart to Enlarge)

Institutions Get Sophisticated

On the institutional side, major brokers are providing their clients with routing technology so that clients can post their own spreads. “Institutional clients are becoming more sophisticated in terms of how they use options,” says Nybo. Though one would expect that “quantitative hedge funds and volatility funds to have done these types of transactions forever,” Nybo says it’s really in the past five or so years that the tech tools have become available, allowing institutional traders to embrace complex order books.

As firms become more options-centric they’ll look for more tools that enable them to do more powerful transactions, perhaps 2,4,6, or 8 sides, says Nybo.

Five years ago, very few front-ends had the capability to trade a spread, he said. “It’s really a whole host of firms that are providing [complex order] functionality,” says Nybo.

Others are seeking access from third-party EMSs, which provide connectivity to all the brokers.

Splitting Orders with Algos

With the fragmentation of complex orders, one way that traders gain an edge is by using algorithms to execute multi-leg strategies across exchange complex order books. In some cases, they are relying on algorithms to manage the complexity of the options strategies.

In Tabb’s options survey, 44 percent of the buy side traders said they used options algorithms to source liquidity, while 31 percent did so to manage complexity, 25 percent to hide intentions, 25 percent for speed and 19 percent for better pricing.

Some execution management systems offer an algorithm in the complex order space, allowing a trader to divide up the order and take a percentage of each complex order book they want to hit.

With algorithms and smart order routers, it’s become easier for buy side firms to execute complex orders. But given the proliferation of complex order books and lack of linkages, there are some challenges.

In Part II next week, we will look at the innovative functionality introduced by options exchanges to enhance executions and seek price improvement as well as market data.

For a complete review of how FlexTrade can help you trade complex order books, please contact us at sales@flextrade.com.